Jacqueline Ferris MacLaren, Esq.

Jacqueline Ferris MacLaren, Esq.

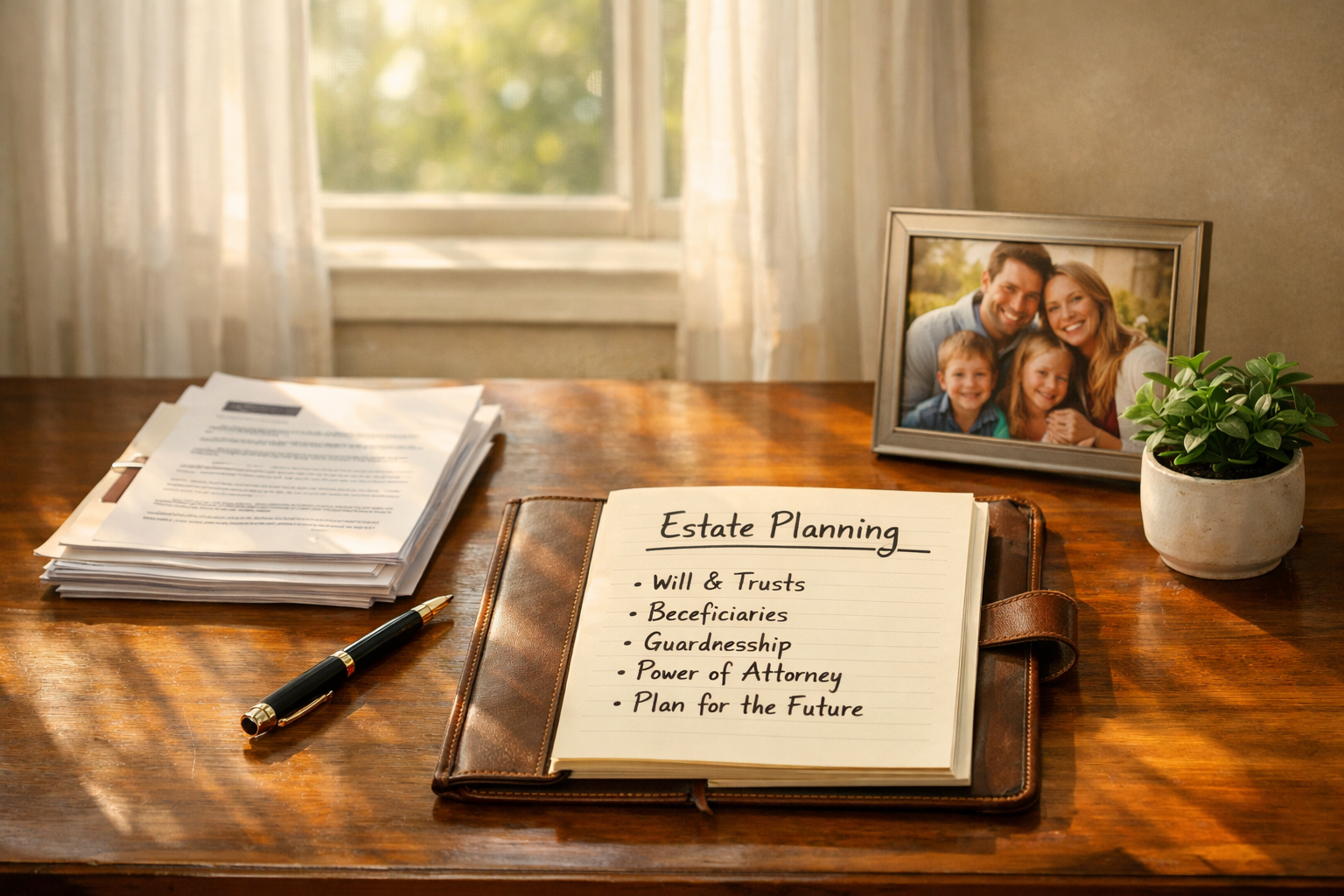

Estate Planning in Ohio: Wills, Trusts & Avoiding Probate

Most people put off estate planning because it feels complicated, expensive, or simply too far off to worry about. The truth is the opposite. A clear...

.png)

At MacLaren Law, LLC, we are committed to keeping you informed about important legal developments that impact your business. Starting January 1, 2024, new federal reporting requirements under the Corporate Transparency Act (CTA) mandate many companies to disclose their beneficial ownership information to the U.S. Department of Treasury's Financial Crimes Enforcement Network (FinCEN).

In light of a recent federal court order, reporting companies are not currently required to file beneficial ownership information with FinCEN and are not subject to liability if they fail to do so while the order remains in force. However, reporting companies may continue to voluntarily submit beneficial ownership information reports. Read on for more information about the events that triggered this change.

The Corporate Transparency Act (CTA) plays a vital role in protecting the U.S. and international financial systems, as well as people across the country, from illicit finance threats like terrorist financing, drug trafficking, and money laundering. The CTA levels the playing field for tens of millions of law-abiding small businesses across the United States and makes it harder for bad actors to exploit loopholes in order to gain an unfair advantage.

On Tuesday, December 3, 2024, in the case of Texas Top Cop Shop, Inc., et al. v. Garland, et al., No. 4:24-cv-00478 (E.D. Tex.), the U.S. District Court for the Eastern District of Texas, Sherman Division, issued an order granting a nationwide preliminary injunction. Texas Top Cop Shop is only one of several cases that have challenged the Corporate Transparency Act (CTA) pending before courts around the country. Several district courts have denied requests to enjoin the CTA, ruling in favor of the Department of the Treasury. The government continues to believe—consistent with the conclusions of the U.S. District Courts for the Eastern District of Virginia and the District of Oregon—that the CTA is constitutional. For that reason, the Department of Justice, on behalf of the Department of the Treasury, filed a Notice of Appeal on December 5, 2024, and separately sought a stay of the injunction pending that appeal.

On December 23, 2024, a panel of the U.S. Court of Appeals for the Fifth Circuit granted a stay of the district court’s preliminary injunction entered in the case of Texas Top Cop Shop, Inc. v. Garland, pending the outcome of the Department of the Treasury’s ongoing appeal of the district court’s order. FinCEN immediately issued an alert notifying the public of this ruling, and recognizing that reporting companies may have needed additional time to comply with beneficial ownership reporting requirements, FinCEN extended reporting deadlines. On December 26, 2024, however, a different panel of the U.S. Court of Appeals for the Fifth Circuit issued an order vacating the Court’s December 23, 2024 order granting a stay of the preliminary injunction. Accordingly, as of December 26, 2024, the injunction issued by the district court in Texas Top Cop Shop, Inc. v. Garland is in effect and reporting companies are not currently required to file beneficial ownership information with FinCEN.

End Update.

This article outlines the key elements of these requirements, including who must file, what information is needed, and critical deadlines to ensure compliance. These regulations aim to enhance transparency and combat financial crimes, but non-compliance can lead to significant penalties.

We encourage you to review this information carefully and reach out to our office for guidance or assistance with your filings. Our goal is to help your business navigate these changes smoothly and effectively.

This correspondence is to make you aware of reporting requirements that went into effect on January 1, 2024, that may require your business entity to report its beneficial ownership information to the Federal government.

The Corporate Transparency Act (“CTA”) expanded anti-money laundering laws and created new reporting requirements for certain companies doing business in the US. Beginning on January 1, 2024, many companies in the United States now have to report information about their beneficial owners, i.e., the individuals who ultimately own or control the company. They now have to report the information to the Financial Crimes Enforcement Network (“FinCEN”). FinCEN is a bureau of the U.S. Department of the Treasury.

NOTE: This is a free filing that companies can complete themselves. Be wary of official-looking mail from a third-party company offering to complete the beneficial ownership reporting on behalf of your company for a fee.

Most businesses, including small businesses, need to file. Your company may need to report information about its beneficial owners if it is:

Reporting companies are to report beneficial ownership information electronically through FinCEN's website: www.fincen.gov/boi.

Beneficial ownership information must be reported for the reporting company’s beneficial owners and (for entities formed or registered after 2023) company applicants. BOI includes an individual’s full legal name, date of birth, street address, and a unique ID number. The unique ID number can be from a non-expired US passport, state driver’s license, or other government-issued ID card. If the individual does not have any of those documents, then a non-expired foreign passport can be used. An image of the document showing the unique ID number must also be included with the report.

Two groups of individuals are considered beneficial owners of a reporting company: (1) any individual who directly or indirectly owns or controls at least 25% of the ownership interests of the reporting company, or (2) any individual who exercises substantial control over the reporting company.

Individuals with substantial control are those with substantial influence over important decisions about a reporting company’s business, finances, and structure. Senior officers (president, CFO, general counsel, CEO, COO, and any other officer who performs a similar function) are automatically deemed to have substantial control, as are individuals with the authority to appoint or remove senior officers and board members. There is no requirement that these individuals have actual ownership in the company to be considered a beneficial owner for reporting purposes.

The penalties for willfully failing to file both the initial and updated reports are steep- $500 per day, if the report is late, up to $10,000, and imprisonment for up to two years.

It will be your exclusive responsibility to comply with CTA, including its BOI reporting requirements. Information can be found at https://www.fincen.gov/boi.

Please call the office at 614-855-6527 or email Jackie at Jackie@maclarenlaw.net with additional questions and/or concerns regarding how BOI reporting requirements and issues affect your company or if you desire assistance with submitting your Company’s BOI report.

If you would like MacLaren Law to assist with filing your BOI report, please complete this FORM and submit it to our office as soon as possible.

We suggest you contact us to assist you with the CTA and related BOI filings for entities you own or control.

📁 Click here to download a copy of this article.

📄 Click here to download the form so MacLaren Law can assist you with this filing.

Whether you're a small business or family-owned, every business needs a plan in place in case something should happen to its owner. Failing to properly plan for your business after your death, whether you are a shareholder, partner, or sole proprietor, can have serious implications on the performance and continuance of your business. Having a proper plan for your business will ensure that your business doesn't have to go through the probate process and can prosper long after you are gone.

Get in Touch Today

IRS CIRCULAR 230 DISCLOSURE:

To ensure compliance with requirements imposed by the Internal Revenue Service, we inform you that any tax advice contained in this communication (including any attachments), was not intended or written to be used, and cannot be used, by any taxpayer for the purpose of (1) avoiding any penalties under the Internal Revenue Code or (2) promoting, marketing or recommending to another party any transaction matter addressed herein.

THE INFORMATION CONTAINED IN THIS TRANSMISSION IS ATTORNEY PRIVILEGED AND/OR CONFIDENTIAL INFORMATION INTENDED FOR THE USE OF THE INDIVIDUAL OR ENTITY NAMED ABOVE. IF THE READER OF THIS MESSAGE IS NOT THE INTENDED RECIPIENT, YOU ARE HEREBY NOTIFIED THAT ANY DISSEMINATION, DISTRIBUTION OR COPYING OF THIS COMMUNICATION IS STRICTLY PROHIBITED. IF YOU HAVE RECEIVED THIS TRANSMISSION IN ERROR, PLEASE IMMEDIATELY NOTIFY ME BY TELEPHONE AND PERMANENTLY DELETE THE ORIGINAL AND ANY COPY OF THIS E-MAIL AND DESTROY ANY PRINTOUT THEREOF.

Most people put off estate planning because it feels complicated, expensive, or simply too far off to worry about. The truth is the opposite. A clear...

You've probably seen the ads: "Create your will in 10 minutes for $39!" And honestly, it's tempting. Estate planning feels like something you...

Creating a will is one of the most important steps in protecting your family and your assets. But a will is not a “set-it-and-forget-it” document....